The Southeast Asia Car Wash Market in 2026: Motorization, Tropical Climate, and the Distributor Opportunity

The Southeast Asia Car Wash Market in 2026: Motorization, Tropical Climate, and the Distributor Opportunity

If you are reading the car wash market Southeast Asia opportunity from outside the region, the shape matters more than a single number. ASEAN is the world's fastest-motorizing major regional bloc, with a fragmented six-nation market that does not fit one figure: Thailand leads on maturity, Indonesia on absolute services value, Malaysia on documented CAGR clarity, Vietnam on car-sales velocity, and the Philippines and Singapore round out the bloc.

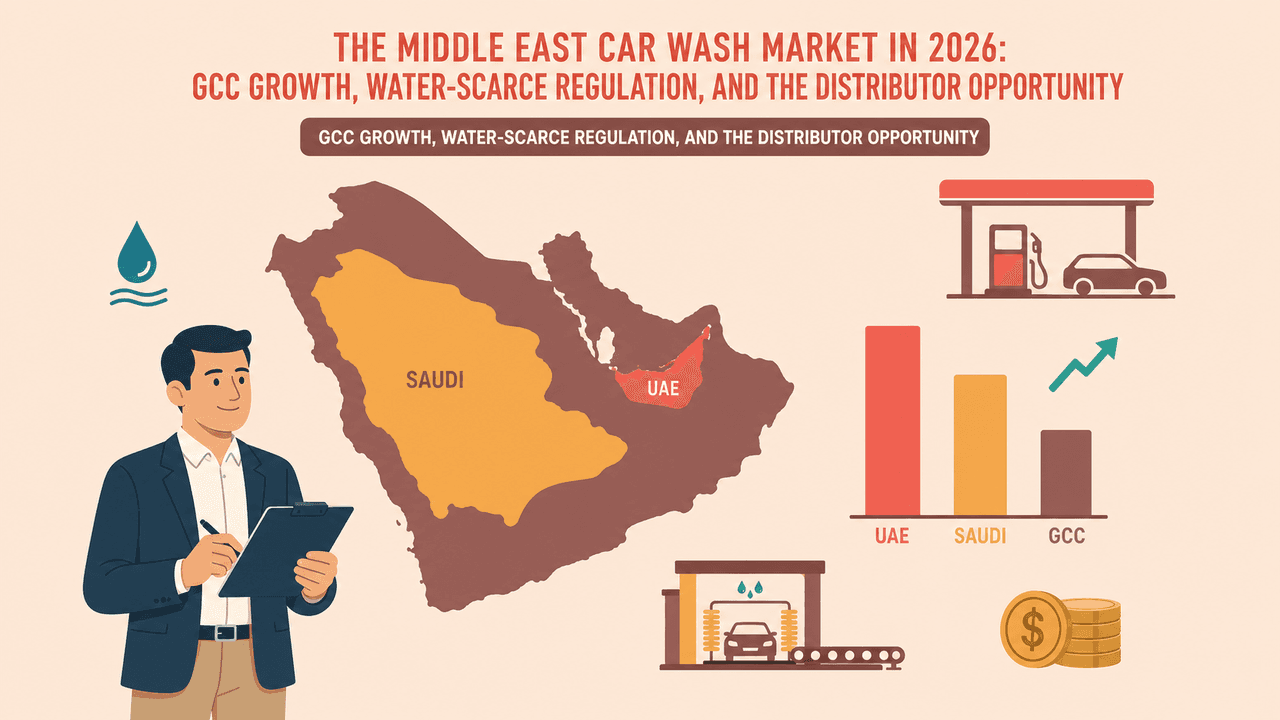

This article is a manufacturer's distributor-perspective primer on the ASEAN market in 2026: size, by-country breakouts, motorization, tropical-climate equipment, franchise-led retail, and equipment-demand implications. It is the third and final piece in a three-part regional series. The US car wash market in 2026 covered a roughly $18.7 billion mature market shaped by chain consolidation. The Middle East car wash market in 2026 covered a roughly $315 million GCC services market shaped by water-scarce regulation and fuel-retail forecourt integration. ASEAN is structurally different from both — smaller in aggregate than the US, larger than the GCC, with motorization as the growth engine and franchise groups as the retail channel that captures it. For broader context, the global car wash equipment market context anchors the ASEAN share within the global category.

How Big Is the Southeast Asia Car Wash Market? Reconciling the Numbers

No single authoritative ASEAN-wide car wash market figure exists in published research; the region is segmented across country-level outlooks that together describe a fragmented market worth several billion US dollars across the bloc in 2025. Mordor Intelligence sizes the broader Asia-Pacific car wash market at USD 6.46 billion in 2024, rising to USD 6.83 billion in 2025 and USD 8.89 billion in 2030 at a 5.40% CAGR. That figure aggregates China, India, South Korea, and other Asia-Pacific markets — including the Rest-of-Asia-Pacific bucket in which ASEAN sits — so it sets a regional ceiling, not the ASEAN floor.

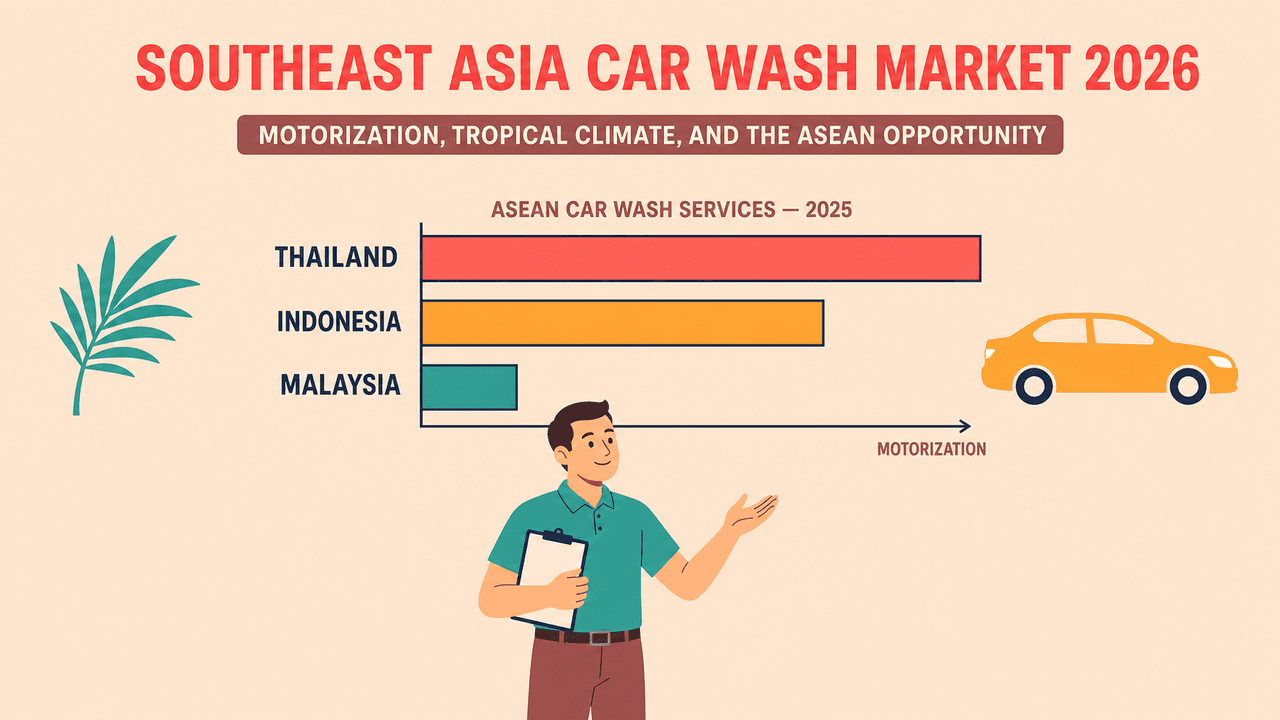

Country anchors fill in the picture. Thailand's car wash market is sized at approximately USD 1.5 billion with a projected 5% CAGR and automated facilities growing at roughly 20% annually. Indonesia's car wash service market is valued at approximately USD 1.1 billion in 2024 per Ken Research. Malaysia's services market sits at USD 208.9 million in 2025, projected to reach USD 361.7 million by 2033 at a 7.3% CAGR; an alternate scope from Markwide Research projects USD 385 million in 2026 rising to USD 639.49 million by 2035 at 5.80% CAGR. Together, documented services revenue across Thailand, Indonesia, and Malaysia is roughly USD 2.8 billion in 2024-2025 aggregate scope.

For context, the US car wash services market is $18.7 billion (IBISWorld 2026) and the GCC sits at $315 million (Mordor 2025). ASEAN lands between the two in absolute size, but ahead of either on motorization-driven growth velocity. Country-level data is fragmented across separate paywalled reports, so equipment-demand inference comes from country-by-country services growth, motorization, and format-mix signals rather than one headline number.

Thailand and Indonesia: Where the ASEAN Car Wash Services Market Is Concentrated

Thailand is the most mature ASEAN car wash market by services value (~USD 1.5 billion) and the strongest automation-adoption signal in the bloc; Indonesia is the largest by services value at the 2024 Ken Research scope (~USD 1.1 billion) and carries the longest vehicle-parc expansion runway. Together the two nations anchor most of the documented ASEAN car wash services revenue and equipment-demand signal.

Thailand Car Wash Market Size and Production Adjacency

Thailand's roughly USD 1.5 billion market is projected to grow at a 5% CAGR, with automated facilities growing at approximately 20% annually — the strongest automation-adoption signal in ASEAN. Thai industry coverage attributes the demand to a 10% rise in car ownership between 2019 and 2023, an expanding middle class, and consistent dirt accumulation in urban centers like Bangkok. Thailand is also ASEAN's automotive production hub — Krungsri Research records more than one million vehicles produced in 2023, the largest in ASEAN — making dealership pre-delivery inspection and service-drive wash a parallel demand stream.

Franchise leadership reflects the maturity. Quik Car Wash positions itself as a turnkey express model with capacity at flagship sites of approximately 2,500 cars per day and a self-dry layout that reduces labor by up to 90% versus traditional Thai operations. International incumbents have visible Thai installations including Leisuwash 360 and SG touchless and Shinewashtec Q14 tunnel — the channel is contested but not closed.

Indonesia Car Wash Market Growth and Franchise Depth

Indonesia operates the largest documented ASEAN car wash services market at approximately USD 1.1 billion in 2024 (Ken Research scope), with vehicle ownership projected to reach roughly 150 million units and urban population at 57% on the long-horizon forecast. Demand concentrates in Jakarta, Surabaya, and Bandung. The broader Indonesian automotive aftermarket service category is projected to reach USD 7.59 billion by 2034 at a 4.78% CAGR — automotive services are a structural growth category, not cyclical.

Franchise depth is the more distinctive Indonesian signal. The top franchise list includes Autoglaze, CARfix, Washteria, AutoBrillo, Masterpiece Car Wash, Dokter Mobil, MobilKlin, GoWash (Gojek's mobile car wash), Auto2000, and Urban Wash, alongside the indigenous manufacturer-cum-franchise PT SATO SARA SEMESTA — which operates the SATO and ROBOTIC CARWASH trademarks and exports car wash equipment to the UAE, Vietnam, Thailand, India, Africa, and Timor Leste. That intra-ASEAN export footprint matters: local manufacturers compete actively against international entrants on price and franchise-channel proximity.

Malaysia's car wash service market sits at USD 208.9 million in 2025 with a documented 7.3% CAGR to 2033, urban concentration in the Klang Valley, and subscription-and-membership models growing fastest among urban consumers. Vietnam is less cleanly sized in published research, but the underlying signal is strong — roughly half a million cars sold in 2024 and a Q2 2025 car-sales surge of 18% year-on-year per Vietnam-Briefing. The Philippines car care products category is projected to grow at a 4.60% CAGR through 2032.

Motorization: Why ASEAN's Car Wash Market Is in Its Early Innings

The single biggest growth driver behind the ASEAN car wash market is motorization — the structural shift from two-wheeler to four-wheeler ownership across the bloc, with the International Trade Administration projecting ASEAN car ownership to rise from 9% (2025) to 30% (2030). Headline car-sales figures are the visible signal; the underlying force is the multi-decade transition of an ASEAN middle class from motorbikes to cars.

Vietnam is the clearest example. Two-wheelers still dominate — more than 74 million were registered as of 2023, over 90% of the motorized fleet, and approximately 3.4 million motorbikes were sold in 2025. But car sales surged 18% year-on-year in Q2 2025 to 90,772 units, on GDP growth of 7.52% in H1 2025 — the highest in 15 years. Vietnam is on track to overtake the Philippines as ASEAN's fourth-largest car market.

Focus2Move records the regional ASEAN vehicle market at 3.25 million units in 2025. Q1 2026 country shares: Malaysia 25.3% (+8.8%), Thailand 22.8% (+17.4%), Indonesia 21.4% (-6%), Vietnam 15.4% (+35.6%), Philippines 13.2% (-6.8%). EV adoption is the structural overlay — 18% of ASEAN sales by Q1 2026 with 67% year-on-year growth, after surging from 9% (2023) through roughly 15% (2024) to the current level. Thailand led ASEAN EV share at 78.7% in early 2023 per Krungsri Research, with Indonesia at 8%.

The equipment-demand implication is straightforward. Motorization is the underlying force that converts ASEAN's vehicle parc growth into car wash equipment demand, and franchise and multi-site chains are the retail channel that captures it at scale. For a distributor evaluating a Vietnam car wash market motorization play, the read is that the country is in the early innings of a structural growth curve, not the late innings of a saturated one.

Tropical Climate and the Equipment It Actually Rewards

The most distinctive structural pressure on ASEAN car wash equipment selection is climate. Unlike the temperate US or the water-scarce GCC, ASEAN equipment operates inside a tropical-monsoon environment that combines three forces a distributor needs to plan for.

The first is humidity. Tropical indoor relative humidity routinely exceeds 85% in ASEAN urban environments against a roughly 50% temperate baseline, and atmospheric corrosion research consistently reports a high corrosion rate of metals under those conditions — moisture accelerates oxidation of chassis, brush assemblies, and electronics enclosures. The second is dust and monsoon rain. Wind-blown dust and seasonal rain leave grit on vehicle paint, which then gets dragged across the surface in the wash cycle if the brush specification cannot resist grit carryover. The third is duty cycle. Unlike temperate climates with seasonal slowdowns, ASEAN equipment runs at near-constant year-round duty, amplifying wear.

Regulation compounds the engineering case. Indonesia, Malaysia, Thailand, and Vietnam each operate their own Water Quality Index frameworks; industrial wastewater discharge requires treatment per zone-level regulations; Malaysia's Department of Environment maintains specific wastewater-discharge guidance for car wash operations. Vietnam's Decree 53/2024/ND-CP (16 May 2024) tightens the operating envelope further. Markwide notes that waterless wash technologies are expanding fastest in Malaysia under exactly these pressures.

The equipment-demand implication is concrete. The ASEAN operator favors equipment built for tropical-monsoon duty: corrosion-resistant stainless components, electronics enclosures with appropriate ingress-protection ratings, brush systems that resist grit carryover (EVA closed-cell foam outperforms older PE foam and bristle because it does not absorb water or trap dirt in its pores), integrated water recycling, and modular configurations serviceable without specialist tools. For more on the brush-free angle relevant to premium franchise concepts, see touchless car wash systems — technology and when to choose; for the broader water-and-energy dimensions, see sustainable car wash operations — water, energy, and ISO 14001.

Franchise and Multi-Site Standardization: ASEAN's Dominant Car Wash Retail Channel

ASEAN car wash retail at scale is franchise-led, not fuel-retail-led as in the GCC and not corporate-chain-led as in the US. Franchise groups and multi-site operators standardize equipment across rollouts that span single-city clusters in Thailand and Malaysia and multi-island networks in Indonesia.

Thailand's franchise leadership runs from Quik Car Wash at the high-throughput express end through Leisuwash and Shinewashtec dealer-channel installations populating the mid-market. Indonesia's franchise depth is unusually wide: Autoglaze, CARfix, Washteria, AutoBrillo, Masterpiece Car Wash, Dokter Mobil, MobilKlin, GoWash by Gojek, Auto2000, and Urban Wash compete for the urban detailing dollar, alongside the manufacturer-franchise hybrid SATO ROBOTIC CARWASH exporting car wash equipment across the ASEAN belt and beyond.

Malaysia tilts toward subscription and membership models — Markwide Research identifies these as the fastest-growing service structure among urban consumers, with mobile car wash also rotating up the share rankings. Vietnam and the Philippines are less franchise-mature, and franchise growth in both tracks the four-wheeler ownership curve.

For a distributor, the channel structure reshapes the account-acquisition motion. Serving the car wash business opportunity Thailand Vietnam landscape requires accounts at the franchise-group procurement level, not standalone-operator level. That means manufacturer support for multi-site standardization across different climate zones, guaranteed parts availability across dispersed networks, and partnership terms that match a multi-site rollout sales motion rather than a one-bay-at-a-time conversation. A car wash franchise ASEAN account is a fundamentally different motion from a US chain account or a GCC forecourt account. For fleet adjacencies the franchise channel does not cover, bus and truck wash systems for fleet operators addresses the parallel stream.

What the Southeast Asia Car Wash Market Means for International Equipment Manufacturers and Their Distributor Partners

Pulling the threads together: the ASEAN car wash equipment market is fragmented across six core nations rather than concentrated in one, smaller than the US in absolute aggregate but with a structurally younger motorization curve, shaped by tropical-monsoon-climate equipment selection pressures, and approached through franchise-group and dealer-channel relationships rather than direct-to-operator or fuel-retail forecourt motions.

Incumbent positions are held by Chinese export-oriented manufacturers including Leisuwash, Shinewashtec, and Risense (active in Thailand and across the bloc), plus the regional manufacturer-franchise SATO ROBOTIC CARWASH exporting intra-ASEAN. European incumbents WashTec, Otto Christ, and ISTOBAL hold positions through distributor networks but are less ASEAN-dominant than in the GCC. Structural openings for international manufacturers sit in four areas: CE and ISO certification baseline that matches ASEAN tender norms; full product range covering touchless, paint-safe brush rollover, conveyor tunnel, fleet, and custom-engineered options; climate-engineered equipment with proof points in tropical-monsoon deployments; and distributor-and-franchise-friendly partnership terms.

We come at ASEAN with three decades of car wash engineering behind us. Nanjing Haiying Machinery has been building these systems since 1992, and the combined HyTian platform has placed 20,000+ systems across 40+ countries, with annual production capacity of 3,000 units from our Nanjing Binjiang facility. Our certifications — ISO 9001, ISO 14001, and CE — match the baseline ASEAN tenders typically expect, and our product range covers the full mix the region needs: paint-safe brush rollover, touchless, conveyor tunnel, bus and truck wash, wheel wash, and engineered-to-order custom builds.

ASEAN is part of our footprint today. We've delivered equipment to clients across Thailand, Vietnam, Malaysia, Indonesia, and other markets in the bloc — every shipment adds to the technical and operating know-how we bring to the next deployment in the region. Regional subsidiaries today operate in the United States, Australia, and Zambia; ASEAN coverage runs through direct client engagements rather than a formal in-region network, and that's the conversation we're actively having with operators, franchise groups, and prospective channel partners looking at the bloc. For distributor and franchise partners thinking through what an equipment-side relationship looks like, the manufacturer partnership guide walks the evaluation framework.

Key Takeaways

No single ASEAN-wide car wash figure exists in published research — the region is fragmented. Key country anchors: Thailand ~USD 1.5 billion (5% CAGR, automated 20%/year), Indonesia USD 1.1 billion (Ken Research 2024), Malaysia USD 208.9 million (Grand View, 7.3% CAGR to 2033). More than USD 2.8 billion in aggregate services revenue across the three.

Motorization is the underlying growth force — ASEAN car ownership projected to triple from 9% (2025) to 30% (2030) per the International Trade Administration, with Vietnam's Q2 2025 car sales +18% YoY and Thailand's 1M+ vehicles produced in 2023 leading the structural shift.

Tropical climate is the equipment selector — humidity above 85% indoors, monsoon-driven grit, and year-round duty cycles reward corrosion-resistant materials, EVA closed-cell foam brushes, and integrated water recycling. Wastewater regulations across Indonesia, Malaysia, Thailand, and Vietnam tighten the envelope further.

Retail at scale is franchise-led, not fuel-retail-led — Quik Car Wash, Autoglaze, SATO ROBOTIC CARWASH, AutoBrillo, GoWash, and dozens more define a franchise-and-multi-site standardization channel structurally different from the GCC and US models.

The distributor opportunity is real but franchise-mediated — entry requires CE and ISO certification, full-range product portfolio with climate-engineered evidence, and partnership terms that match a multi-site franchise standardization sales motion rather than direct-to-operator.

Talk to Our Partner-Development Team

Evaluating the ASEAN car wash equipment market as a distributor or franchise partner? Our team can walk you through the regional opportunity, climate-engineered product fit, certification baseline for ASEAN tenders, and what a HyTian partnership looks like in practice. Start with the manufacturer partnership guide above, then talk to our partner-development team about your territory.

Start a conversation: Request a quote or talk to our partner-development team about your ASEAN territory.

Related articles

Explore more insights from the HyTian team.

The US Car Wash Market in 2026: Size, Format Share, and the Distributor Opportunity

The US car wash market size reached $18.7B in 2026 — here's the format share, regional concentration, and equipment-demand picture a manufacturer sees.

The Middle East Car Wash Market in 2026: GCC Growth, Water-Scarce Regulation, and the Distributor Opportunity

The GCC car wash market reached USD 315M in 2025 — here is the by-nation growth, water-scarce regulation, and equipment-demand picture a manufacturer sees.

The Global Car Wash Equipment Market: Size, Growth, and Opportunity by Region

Car wash equipment market size and regional growth through 2031 — a distributor's view from a manufacturer with 20,000+ systems in 40+ countries.